How Compound Interest Doubling Works: A Rule-of-72 Walkthrough for Real Savings Accounts

Last updated: May 04, 2026

Divide 72 by your annual rate of return and the result is roughly the number of years it takes a lump sum to double. At a 4.50% APY high-yield savings account, that’s about 16 years. The catch is that nearly every explainer stops there. A real saver in a taxable account, paying federal tax and losing ground to inflation, will not see their purchasing power double in 16 years — or anywhere close. The rule needs three corrections before it earns a place on your fridge.

- Formula: years to double ≈ 72 ÷ annual rate (entered as a percent, not a decimal).

- Error stays under 0.3 years for rates between 4% and 12% — exactly the band consumer savings products live in.

- Apply the rule to your after-tax, after-inflation rate, not the headline APY a bank advertises.

- For rates under 2% use 69.3; above 15% drop the rule and run an actual calculator.

- The rule assumes one lump sum at a fixed rate. It cannot model monthly deposits or APY resets.

The Rule of 72 in 30 Seconds — and the Three Corrections Most Guides Skip

The rule of 72 explained in one line: 72 ÷ rate = years to double. At 6% you double in 12 years; at 9% in 8; at 4.50% in 16. The math comes from a clean approximation of the exact doubling formula t = ln(2) / ln(1 + r). The U.S. Securities and Exchange Commission’s investor education arm, Investor.gov’s compound interest calculator, runs the exact version of this calculation if you want to see it without the shortcut.

The three corrections most articles skip:

- APY vs nominal. Banks quote APY, which already includes intra-year compounding. Plug APY into the rule, not the stated nominal rate, or you will overstate doubling time by the spread between them.

- After-tax, after-inflation. A 4.50% APY in a taxable account at the 24% federal bracket nets you about 3.42%. Subtract 3% inflation and your real rate is roughly 0.4% — a doubling time that runs into multiple human lifetimes.

- The rule assumes a lump sum. If you contribute $200 a month, your balance will pass any “doubled” target faster than the rule predicts, but only because new principal is showing up — not because compounding got better.

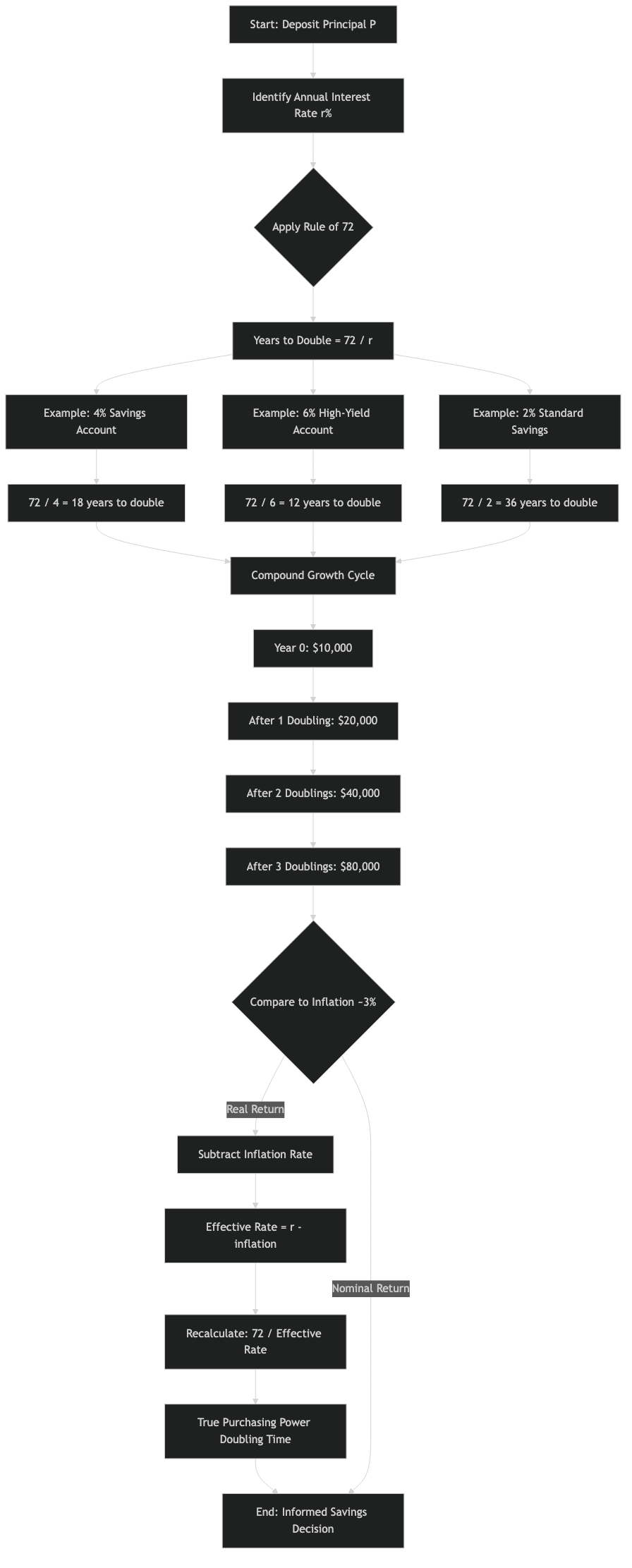

Purpose-built diagram for this article — How Compound Interest Doubling Works: A Rule-of-72 Walkthrough for Real Savings Accounts.

The diagram above traces a single dollar through the doubling math: it starts at the headline APY, gets shaved by federal tax, then by inflation, and only the surviving sliver is what compounds in real terms. The point of the picture is that the gap between the marketing rate and the doubling-power rate is much larger than most savers expect.

Why It’s 72 and Not 69.3: The Accuracy Sweet Spot

The exact answer to “when does my money double” is t = ln(2) / ln(1 + r). Because ln(2) ≈ 0.6931, a perfectly accurate shortcut for very small rates would be 69.3 ÷ rate. So why does everyone teach 72?

Two reasons. First, 72 is divisible by 1, 2, 3, 4, 6, 8, 9, and 12 — handy for mental arithmetic at almost any common interest rate. Second, the linear approximation ln(1+r) ≈ r becomes worse as r grows. Bumping the numerator from 69.3 up to 72 compensates for that drift, and the two errors cancel out almost perfectly somewhere around 8%.

That gives the rule a measurable accuracy band. Compare the rule’s output to ln(2)/ln(1+r) across the rates a U.S. saver actually sees on deposit products today:

| Annual rate | Rule of 72 estimate | Exact doubling time | Error (years) | Typical product at this rate |

|---|---|---|---|---|

| 0.50% | 144.0 | 138.98 | +5.02 | Big-bank checking sweep |

| 1.00% | 72.0 | 69.66 | +2.34 | Legacy savings account |

| 2.00% | 36.0 | 35.00 | +1.00 | Short Treasury bill |

| 3.75% | 19.20 | 18.83 | +0.37 | Lower-tier HYSA, May 2026 |

| 4.50% | 16.00 | 15.75 | +0.25 | Marcus / Ally HYSA tier |

| 5.00% | 14.40 | 14.21 | +0.19 | Top-tier HYSA / 12-month CD |

| 5.25% | 13.71 | 13.55 | +0.16 | Brokered CD ladder rung |

| 7.00% | 10.29 | 10.24 | +0.05 | Long-run bond fund estimate |

| 10.00% | 7.20 | 7.27 | −0.07 | S&P 500 long-run nominal |

| 15.00% | 4.80 | 4.96 | −0.16 | Above the rule’s reliable band |

Source: doubling time computed as ln(2) ÷ ln(1+r); rate examples cross-checked against the Federal Reserve H.15 selected interest rates and posted HYSA rates as of May 2026.

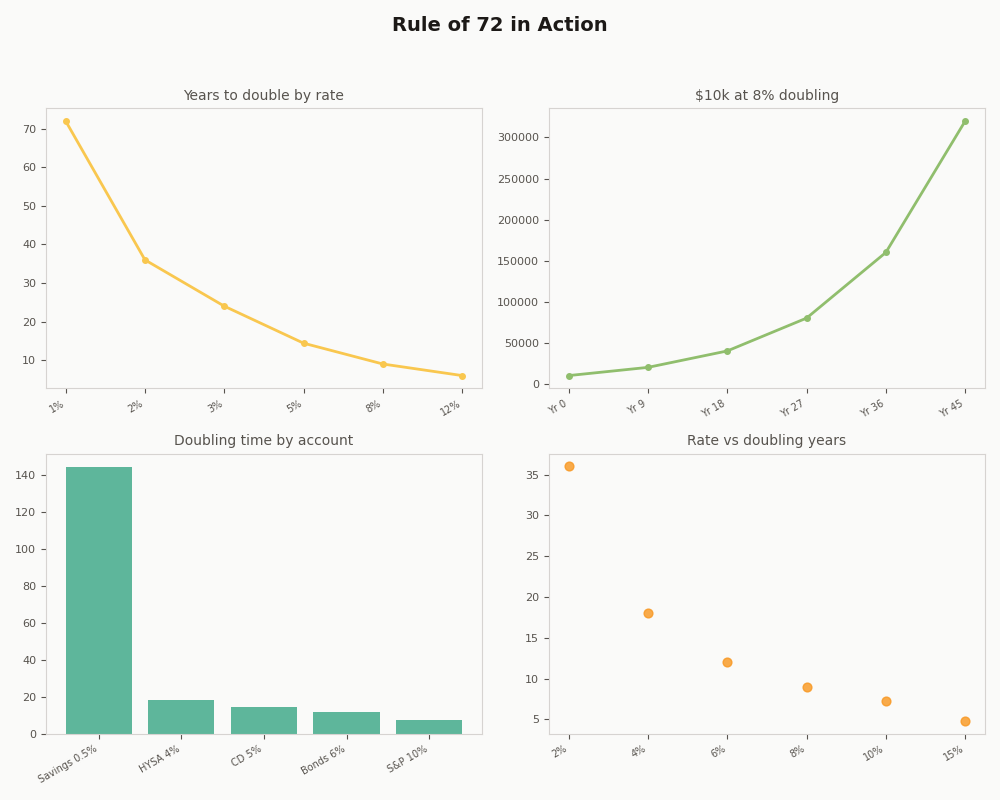

The pattern is the opposite of what some explainers say. The rule’s accuracy is worst at very low rates (over 5 years off at 0.5%) and excellent in the 4% to 12% sweet spot. That happens to be the band most consumer savings products live in, which is why 72 became the default in the first place.

Plugging in a Real Savings Account: APY vs Nominal Rate

Banks display APY because federal Truth in Savings rules require it — and APY already factors in monthly or daily compounding. The Rule of 72 expects an effective annual rate. That means: plug in APY directly. If you mix up APY and the nominal rate, you’ll overstate doubling time by a small but meaningful amount.

Worked example. A 4.50% APY HYSA on a $10,000 deposit. Using the rule: 72 ÷ 4.5 = 16.0 years. The exact compound math says 15.75 years. Tiny error. Now suppose someone confuses APY with the nominal rate and assumes 4.50% means simple interest. Simple interest on $10,000 at 4.5% would take 22.2 years to double — almost six and a half years too long. The mistake is not in the rule; it’s in the input.

More detail in clean up your money stack.

One more landmine: tiered APY. Some HYSAs pay 4.50% only up to a balance cap (commonly $25,000 or $250,000) and a much lower rate on the excess. If your balance straddles the cap during the doubling window, the blended effective rate is lower than the headline, and the rule gives you the wrong answer until you weight it by tier.

After-Tax, After-Inflation: The Doubling Time That Actually Matters

Doubling dollars is easy. Doubling purchasing power is the harder problem, and it’s the only one your future self cares about. Two adjustments turn the headline APY into a real rate:

- Tax. HYSA interest is ordinary income at your federal marginal bracket plus state. The IRS publishes the bracket schedule each year; the 2026 ordinary-income brackets are listed in the IRS Publication 17. A single filer making $70,000 hits the 22% federal bracket; at $110,000 they hit 24%.

- Inflation. The Bureau of Labor Statistics publishes the CPI-U monthly. The trailing 12-month figure as of the most recent BLS CPI release is the right benchmark for a saver thinking about a one-year horizon.

Now run the same 4.50% HYSA, $10,000, 24% federal bracket, no state tax, 3.0% inflation:

There is a longer treatment in offsetting taxable gains.

| Layer | Effective rate | Years to double (Rule of 72) |

|---|---|---|

| Headline APY | 4.50% | 16.0 |

| After 24% federal tax | 3.42% | 21.1 |

| After 24% tax and 3.0% inflation | ≈ 0.41% | ≈ 176 |

Real rate calculated as (1 + after-tax rate) ÷ (1 + inflation) − 1, the Fisher relation, not the lazy subtraction.

That last row is the number savings-account marketing copy never shows. At a 24% bracket and 3% inflation, a 4.50% HYSA roughly preserves purchasing power; it does not meaningfully grow it. If inflation runs at 3.5% — which the CPI-U has done in long stretches — the real rate goes negative and the rule mathematically blows up.

This is also where account placement matters. The same 4.50% earned in a Roth IRA skips the tax row entirely; in a Traditional IRA the tax is deferred but still owed at withdrawal. Series I Savings Bonds, documented at TreasuryDirect’s I-Bond page, defer federal tax until redemption and exempt state tax — a meaningful boost to the after-tax row, although they cap purchases at $10,000 per Social Security number per year.

When the Rule Lies: Variable Rates and the HYSA Reset Problem

The rule wants one rate for the whole holding period. Real high-yield savings accounts reset their APY whenever the bank decides — usually within a week or two of a Federal Reserve rate move. Marcus by Goldman Sachs, Ally Online Savings, Discover, and Synchrony all reprice through cycles. That makes any single-rate input a snapshot, not a forecast.

Look at the rough APY arc of a typical online savings account from January 2022 through May 2026:

- Early 2022: well under 1% APY across most online banks while the Fed funds rate sat near zero.

- Through 2023: APYs climbed past 4% as the Fed lifted the funds rate above 5%.

- 2024 plateau: APYs stabilized in the 4.25%–5.00% range across the top tier.

- Late 2024 into 2026: APYs drifted lower as the Fed began cutting; top-tier HYSAs are commonly 3.75%–4.25% by May 2026.

A saver who looked at the 4.50% peak and ran 72 ÷ 4.5 = 16 years was implicitly assuming the peak rate would hold for 16 years. The trailing four-year geometric mean across that same window sits closer to 3.0%, which gives a doubling estimate of 24 years — eight years longer than the snapshot answer. The Federal Reserve’s H.6 money stock release and the FDIC weekly national rate data both let you reconstruct these averages from primary data.

The practical fix: never run the rule on the current advertised rate alone. Run it twice — once on today’s APY for a best-case bound, and once on a reasonable trailing average for a more honest center.

The architecture above maps that workflow: real APY data flows in, an averaging window smooths it, and only then does the rule produce two bounded estimates instead of one false-precision number. The rule itself is a calculator, not a forecaster — pairing it with rate history is what makes the output trustworthy.

When the Rule Lies: Lump Sums vs Monthly Contributions

The rule answers exactly one question: when does this dollar, sitting still, double in nominal terms? It cannot answer a different and more interesting question: when does my balance double if I keep adding to it?

Compare two savers, both starting at $10,000 with a 5.00% APY account:

trimming weekly spend goes into the specifics of this.

| Scenario | Year 5 balance | Year 10 balance | Year 14.4 balance | When balance hits $20,000 |

|---|---|---|---|---|

| $10,000 lump sum, no contributions | $12,763 | $16,289 | $20,003 | 14.4 years (the rule’s answer) |

| $10,000 lump sum + $200/month | $26,367 | $47,373 | $70,690 | ≈ 3.6 years |

Calculations assume monthly compounding at a 5.00% APY (≈ 4.889% nominal, monthly). Balances rounded to the nearest dollar.

The contributing saver’s balance “doubles” in under four years, but only because they added $8,640 in fresh deposits during that window. Their original $10,000 still takes the same 14.4 years to double on its own. Confusing the two is how people convince themselves a savings account is growing faster than it is — the deposits are doing most of the work, not the interest.

If you want a single number for a contribution plan, the rule is the wrong tool. A future-value-of-an-annuity calculation does the job, and the SEC’s free compound interest calculator handles monthly deposits without making you derive it.

Pick Your Rule: 72 vs 69.3 vs 70 vs 78 by Rate Band

The rule of 72 has cousins. Each numerator works best in a specific rate band:

| Rate band | Best numerator | Max error in years (within band) | Use case |

|---|---|---|---|

| Below 2% | 69.3 | ≈ 0.4 | Big-bank savings, short Treasuries during low-rate cycles |

| 2% – 4% | 70 | ≈ 0.5 | Lower-tier HYSAs, money-market funds, short CDs in soft cycles |

| 4% – 12% | 72 | ≈ 0.3 | Top-tier HYSAs, CDs, I-Bonds, long-run stock returns |

| 12% – 18% | 76 or 78 | ≈ 0.4 | High-yield credit, leveraged returns, hyperinflationary scenarios |

| Above 18% | None — use ln(2)/ln(1+r) | n/a | The shortcut error grows past one full year; run the exact formula |

For the rate a typical U.S. saver actually faces — anywhere from a 0.40% checking sweep to a 5.25% brokered CD — the right choices are 69.3, 70, or 72 depending on which side of the 4% line you’re on. If you only want to remember one, 72 stays within a year of correct across nearly every consumer scenario, which is why it’s the version that survived from Luca Pacioli’s 1494 Summa de Arithmetica through to modern finance textbooks.

Decision Framework: Which Tool for Which Question

The rule is a hammer. Most savings questions are screws. Use this checklist to pick the right instrument before you do any math:

- Choose the Rule of 72 if you have a single lump sum, a roughly stable rate between 4% and 12%, and you only need an answer accurate to within a few months. Mental-math friendly; no calculator needed.

- Choose 69.3 instead of 72 if your rate is under 2% (legacy savings accounts, big-bank checking sweeps, low-cycle Treasuries). At those rates the standard rule overstates doubling time by years, not months.

- Choose 70 instead of 72 if your rate sits between 2% and 4% (lower-tier HYSAs, money-market funds, short CDs during soft cycles) and you want the smallest possible error without giving up easy mental math.

- Choose 78 (or skip the rule entirely) if your rate is above 12% — high-yield credit, leveraged returns, or any back-of-envelope inflation modeling. The shortcut drifts past a full year and stops being trustworthy.

- Pick the exact formula t = ln(2) / ln(1 + r) if you need precision better than ±0.3 years, your rate is below 1% or above 15%, or you’re presenting numbers to anyone who will check them.

- Pick a future-value-of-an-annuity calculator (or the SEC’s compound interest calculator) if you make recurring deposits. The rule is contribution-blind; it cannot tell you when a balance with monthly contributions will double, and the answer it gives will be off by years.

- Pick a rate-history average — not today’s APY — if you’re modeling a variable-rate product (HYSA, money-market fund, floating CD). Run the rule twice: once on the current rate as a best-case bound, once on a 3-to-5-year trailing average as the realistic center.

- Pick the after-tax, after-inflation real rate (not the headline APY) if the question is about purchasing power instead of nominal dollars — which it almost always is for a personal saver. Apply the Fisher relation, not lazy subtraction.

- Skip the rule entirely if the rate is variable and contributions are recurring and taxes apply. At that point you have three sources of error stacked on top of each other and only a real spreadsheet or calculator will give you a number worth trusting.

The shortest version: use the rule when you have one dollar, one rate, and one decade. Reach for a calculator the moment any of those three assumptions breaks.

The Sober Takeaway: What ‘Doubling’ Buys You in 2026

Pull all of it together for the products a saver can buy today. Apply Rule of 72 first to the nominal rate, then to a real after-tax rate at a 24% federal bracket and 3.0% inflation:

| Product | Representative rate | Nominal doubling (Rule of 72) | After-tax, after-inflation doubling |

|---|---|---|---|

| Top-tier HYSA | 4.25% APY | 16.9 years | essentially never (real rate ≈ 0.13%) |

| 12-month brokered CD | 5.00% APY | 14.4 years | ≈ 92 years |

| Series I Savings Bond (composite) | ~3.50% (state-tax exempt, federal-tax deferred) | 20.6 years | ≈ 144 years (taxes deferred, not avoided) |

| S&P 500 in a Roth IRA | 10% nominal long-run | 7.2 years | ≈ 10.3 years (no tax row; 7% real) |

| S&P 500 in a taxable brokerage | 10% nominal, 15% LTCG, 3% inflation | 7.2 years | ≈ 13.0 years |

Long-run S&P figure based on the Damodaran historical equity premium dataset; LTCG rate per the IRS published rate schedule for taxpayers in the middle bracket band.

More detail in planning around big life milestones.

The dashboard view above is the version of this table a saver should actually keep nearby: the leftmost column shows what the bank advertised, and the rightmost column shows what the dollar will actually buy when it doubles. The widening gap from left to right is the entire reason the Rule of 72 needs the three corrections — without them, it’s an optimism machine.

Two practical upshots. If your goal is to preserve purchasing power, a HYSA in a taxable account at the current rate band can do that, but barely; a tax-advantaged account makes the same APY meaningfully more useful. If your goal is to actually double real purchasing power inside a working career, the rule is telling you something important: deposit-rate products cannot do it on their own at typical brackets and typical inflation. You need either a tax-sheltered wrapper, a higher-return asset class, or — most realistically — both.

If you want to keep going, how equity comp gets taxed is the next stop.

the resale economy in 2026 is a natural follow-up.

Further reading

- SEC Investor.gov: Compound Interest Calculator — the official exact-math version of the doubling calculation, free to use.

- Federal Reserve H.15: Selected Interest Rates — primary source for the historical Treasury and money-market rates referenced in the rate-band table.

- U.S. Bureau of Labor Statistics: Consumer Price Index — the inflation series to use when computing your real rate.

- TreasuryDirect: Series I Savings Bonds — official rules for I-Bond composite rates, federal tax deferral, and the $10,000 annual purchase limit.

- IRS Publication 17 — current marginal bracket schedule used in the after-tax calculations above.

- Encyclopaedia Britannica: Luca Pacioli — biography of the 15th-century mathematician credited with the earliest known printed mention of the rule.

You may also like

Leave a Reply